Mainland Chinese medium- and major-obligation vehicles (MHDTs) have

entered a bear market because mid-2021. While the market place staged a

slight restoration adhering to the easing of electric power shortages and

injection of plan stimulus from late final yr, unforeseen

headwinds brought by the Russia-Ukraine crisis and domestic Omicron

outbreak plunged the industry back again into weak spot in the second

quarter of 2022. Amid pandemic-induced lockdowns in Jilin and

Shanghai, creation of MHDT strike the lowest examining for April more than

a decade. In our Could forecast, we downgraded the mainland Chinese

MHDT manufacturing for 2022 by 5% to 1.13 million models, a drop of

23% compared with 2021.

External geopolitical tensions push up producer fees

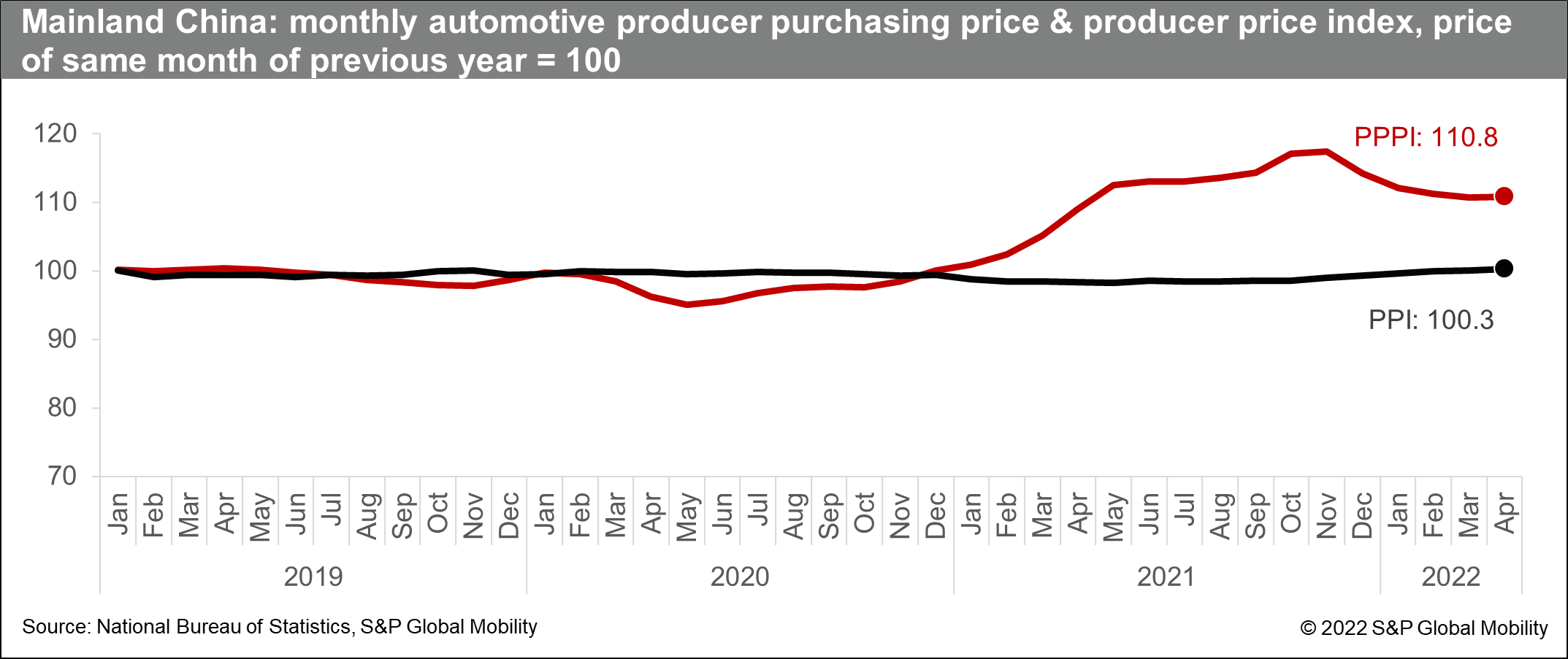

As uncooked elements characterize 20-30% of the expense of output for

weighty vans, raw product fees partly decide the

profitability of truck producers. Owing to the world-wide financial

restoration from the COVID-19 scare, commodity charges have

gone through an upcycle considering the fact that late 2020. The rally acquired much more steam

in the to start with quarter of 2022 with the outbreak of the

Russia-Ukraine war. Specially, the chilly-rolled metal price that

accounts for above 60% of the whole uncooked content costs for a heavy

truck surged by 3% in March 2022 from the level of January,

expanding the progress to extra than 40% as in contrast to the very same

period of time of 2020. Also, the diesel value elevated by 15% and passed the

RMB9,000 for each metric ton mark by way of January-March 2022. In

contrast, the movement of selling price ranges for significant trucks had been

instead flat less than slack need, as fuel rate inflation elevated

the functioning expenses when oversupplied trucking constrained freight

level advancement. As a final result, the truck producers’ acquiring and

promoting price ranges logged considerable differentiation, irrespective of an

improve in rate of CN6-level designs. Such weak inflation

move-by means of impact has made truck makers to bear the brunt of the

income margin squeeze especially just after dumping of CN5-degree vans.

With the Russia-Ukraine crisis expected to deepen into 2023,

limited-time period truck generation is thus cut by all around 25,000 units

in the Might outlook.

Inside pandemic resurgences exacerbate source chain

disruptions

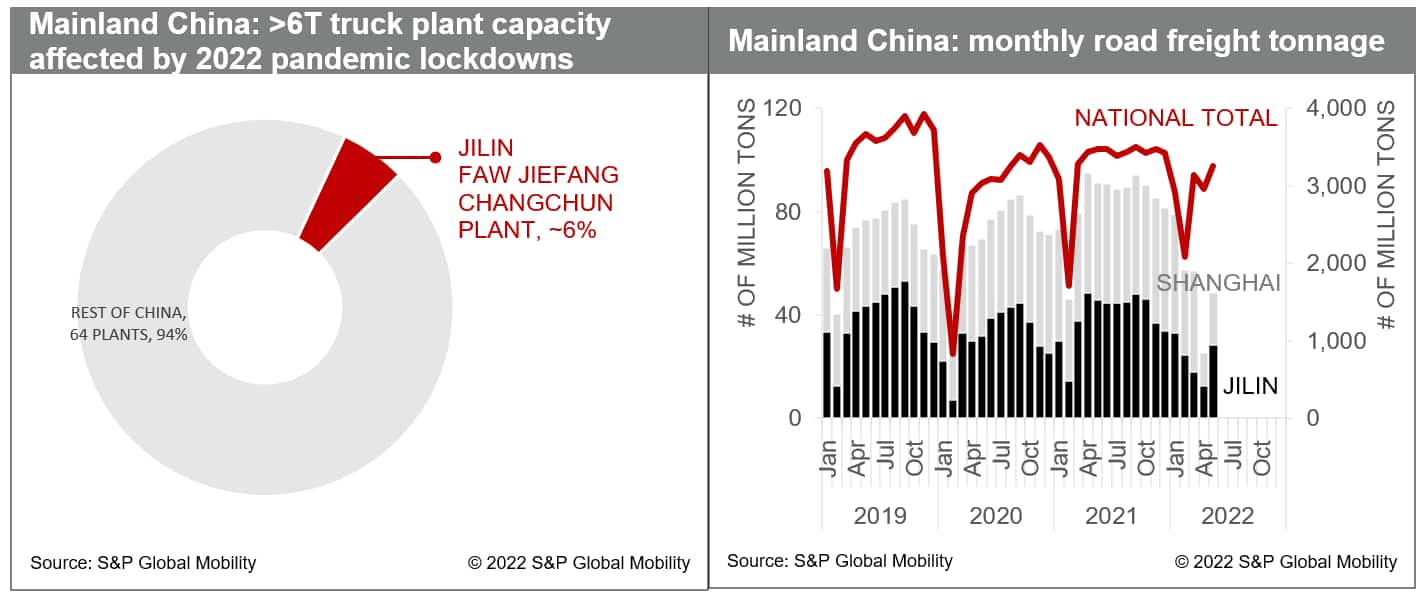

The Omicron wave experienced brought on large lockdowns in Jilin

Province (March 11-April 28), Shenzhen City (March 14-20), and

Shanghai Town (March 28-Could 31) given that March 2022, ensuing in

common organization disruptions and logistics snarls. Even though

there are few MHDT makers in the epicenters of the pandemic,

Changchun Town and Shanghai Metropolis host around 40 significant offer bases

serving core components to mainstream versions covering previously mentioned 90% of

truck production. Commencing from mid-April, FAW Jiefang’s Changchun

plant and most suppliers managed to resume work in the closed-loop

technique, but labor shortages below the mobility control disabled

them to purpose at normal capability. In the meantime, rigorous

containment steps this kind of as visitors constraints, nucleic acid

test and quarantine requirements, as properly as closure of toll

stations pent up road freight demand and prompted wider repercussions

of part shortages, which in switch dampening truck manufacturing.

Underneath the situations, the complete reduction of MHDT creation in the

next quarter is believed to reach 100,000 units. With ramping up

endeavours to sleek logistics and restore small business, the perform

resumption charge of enterprises previously mentioned designated measurement in Shanghai

Town enhanced to 96% by mid-June and will totally recover from July.

Coupled with expansionary guidelines and adequate capacity

reserves, these could assist MHDT production to decide on up and offset

the pandemic-induced loss in the 2nd fifty percent.

A even further downgrade to outlook is less than assessment, as the

government’s reliance on the “dynamic zero-COVID” tactic and

capital outflows led by the Fed’s tightened cycle are very likely to

weaken enterprise sentiment and subdue demand recovery. On the other

hand, the rebuilding of supplier inventories of CN6-stage MHDTs

climbed from 280,000 models in early this 12 months to 380,000 models by

April, way bigger than the regular premiums of 150,000-170,000 models.

In addition, there were being a lot more than 70,000 units CN5-stage new

vans (bought as applied vehicles) remaining in the current market, exacerbating

de-stocking pressures.

This post was posted by S&P Global Mobility and not by S&P International Rankings, which is a separately managed division of S&P World.

:strip_icc():format(webp)/kly-media-production/medias/1564067/original/014467400_1491964869-Travel-2.jpg)

More Stories

What Documents Are Required For Financing and Buying A Car In Chicago?

Types of Brake Defects

Top 10 Benefits of Having a Car and Driving Licence